Financial markets are moving faster than the risk infrastructure many institutions still rely on, making delayed risk insight increasingly costly. To keep pace, firms are shifting from overnight reporting to AI-driven systems that deliver real-time risk insight, allowing exposure to be evaluated as conditions change throughout the trading day.

Advances in machine learning have enabled deeper simulation and faster scenario analysis, but insight alone is not enough. At intraday scale, AI-powered risk management succeeds or fails based on infrastructure: the ability to deliver predictable, low-latency compute at scale.

This dynamic is already playing out inside the most advanced risk organizations.

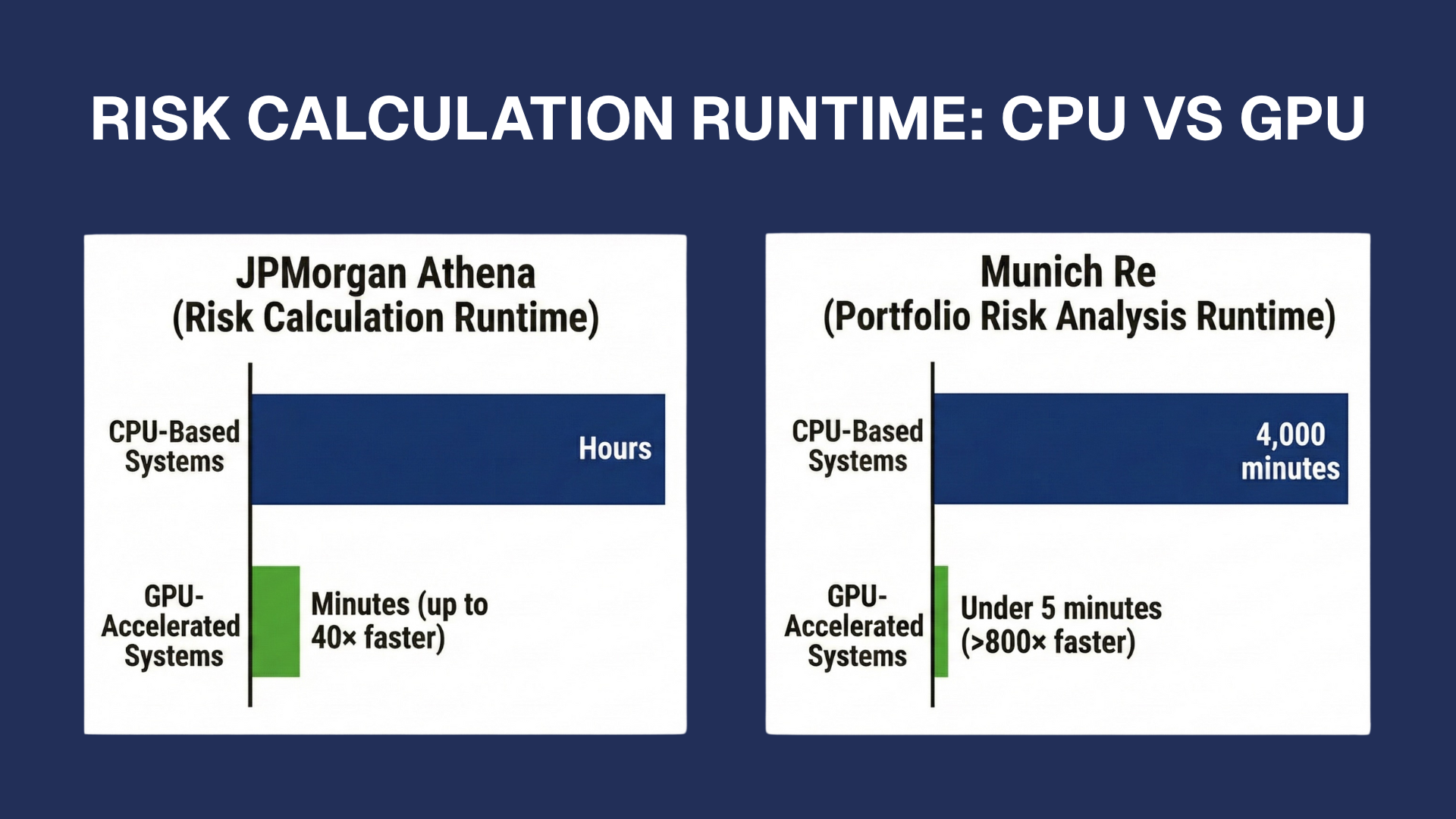

When JPMorgan modernized its Athena risk platform, it was because legacy, batch-based risk infrastructure was becoming a limiting factor in real-time markets. As the scope and frequency of risk calculations increased, CPU-based systems could no longer support timely insight. By moving core risk workloads onto GPU-accelerated infrastructure, the firm achieved performance gains of up to 40x, with risk calculations running in minutes rather than hours.

JPMorgan’s experience reflects a broader shift across financial services. As markets move faster and regulations demand deeper, more frequent risk insight, institutions are moving toward intraday risk management, real-time VaR, and Expected Shortfall under FRTB. AI can make risk models more adaptive, but at intraday scale, infrastructure, not algorithms, becomes the primary constraint.

This article outlines how intraday risk systems are being built, why GPU infrastructure is now central to real-time risk analytics, and what regulated institutions must consider when moving these systems into production.

Why Finance Is Turning to AI for Risk Management

The adoption of AI in risk management is driven less by experimentation and more by structural pressure on existing architectures. Regulatory frameworks such as Basel III and FRTB require risk to be measured with greater granularity, stronger governance, and increased frequency.

The shift from Value at Risk to Expected Shortfall materially increases computational load, particularly when calculations must be refreshed intraday and at the trading-desk level. Producing these metrics continuously is no longer feasible using batch-based workflows.

AI risk modeling helps institutions manage this complexity through large-scale simulation, adaptive recalibration, and richer sensitivity analysis. In regulated environments, however, these techniques only become operational when paired with infrastructure capable of sustaining continuous computation while preserving transparency and control.

Core AI Techniques Supporting Intraday Risk

At intraday scale, familiar risk techniques place fundamentally different demands on infrastructure. Risk management does not rely on new modeling concepts, but the way established methods operate changes materially when calculations must run continuously, respond to live market movement, and remain explainable and auditable under regulatory scrutiny.

As recalculation frequency increases, stress testing and Monte Carlo simulation place sustained pressure on compute. Monte Carlo remains central to market and credit risk, but refreshing simulations intraday sharply raises computational demand. GPU acceleration enables large-scale parallel execution, making continuous recalculation operationally viable in production environments.

These infrastructure demands intensify further under intraday VaR and Expected Shortfall. FRTB-driven Expected Shortfall requires significantly more computation than traditional VaR, particularly when calculated at the trading-desk level and refreshed throughout the day. Delivering these metrics in real time depends on infrastructure that can sustain high-throughput simulation without introducing latency or sacrificing accuracy.

At the same time, continuous execution requires model monitoring and explainability to operate alongside core risk calculations. Techniques such as anomaly detection help surface unexpected changes in risk metrics, while methods such as SHAP support regulatory transparency. These governance workflows add nontrivial computational overhead that must run concurrently without degrading performance.

Together, these demands shift the core challenge of intraday risk management away from model design and toward reliable execution at scale. Compute performance, throughput, and determinism become central to whether AI-powered risk systems can function continuously in regulated production environments.

Why Intraday Risk Depends on Compute

Delivering intraday risk in production places fundamentally different demands on infrastructure than traditional batch-based systems. Real-time VaR and Expected Shortfall require continuous simulation, low-latency execution, and predictable performance under sustained load. As these calculations move from periodic reporting into live decision-making, infrastructure must support not only speed and scale, but also transparency, control, and reproducibility.

In regulated environments, these requirements surface most clearly around explainability at speed. Risk metrics must remain interpretable even as recalculation frequency increases. Techniques used to support explainability add nontrivial computational overhead, which infrastructure must absorb without delaying results or degrading performance.

Production risk systems must also enforce governance and data control. Risk workloads are subject to strict data residency, access control, and audit requirements, often limiting where and how computation can run. This pushes many institutions toward on-prem or hybrid deployments that provide tighter operational control while still supporting continuous recalculation.

Finally, intraday risk depends on latency predictability and audit replay. Institutions must be able to reproduce risk calculations exactly as they ran at a given point in time, including during periods of market stress. Predictable latency and deterministic execution are essential to ensure results can be audited, explained, and trusted by regulators and internal stakeholders alike.

Munich Re Markets: Portfolio Risk at GPU Speed

Munich Re Markets illustrates how GPU infrastructure enables explainable risk analysis at production speed. In a publicly documented workflow, the team evaluated portfolio risk across 100,000 simulated market scenarios and used interpretable machine learning to explain differences in allocation strategies. SHAP was required to meet governance standards and became the primary computational bottleneck.

On legacy CPU infrastructure, the analysis exceeded 4,000 minutes, limiting its usefulness to periodic research. After refactoring the pipeline to a GPU-native stack on an NVIDIA DGX Station with four V100 GPUs, runtime dropped to under five minutes, an improvement of more than 800x. This shift allowed the analysis to move into regular risk workflows while preserving regulatory-grade explainability.

Supporting Production-Grade Risk Systems with Arc Compute

As risk teams move toward continuous, intraday calculation, infrastructure becomes a control layer rather than a supporting service, which is the same inflection point that drove JPMorgan’s modernization of Athena.

Arc Compute provides GPU infrastructure for regulated financial workloads through on-prem and hybrid deployments. These environments deliver predictable performance, support data residency and auditability, and enable AI-powered risk systems to run reliably at scale. As intraday risk becomes the default operating model, infrastructure choices will increasingly determine which institutions can translate AI insight into real-time, trusted decision-making.

References

How JPMorgan Chase Modernized Its Core Risk Platform

Market Risk Platforms and Paradigms: Basel III Compliance and GenAI Integration

GPU Monte Carlo Acceleration Discussion

Accelerating Interpretable Machine Learning for Diversified Portfolio Construction